Sustainable investment in Europe: Trends and prospects

Rédigé par Amadou Kasse Publié le 17/01/2025

Partager

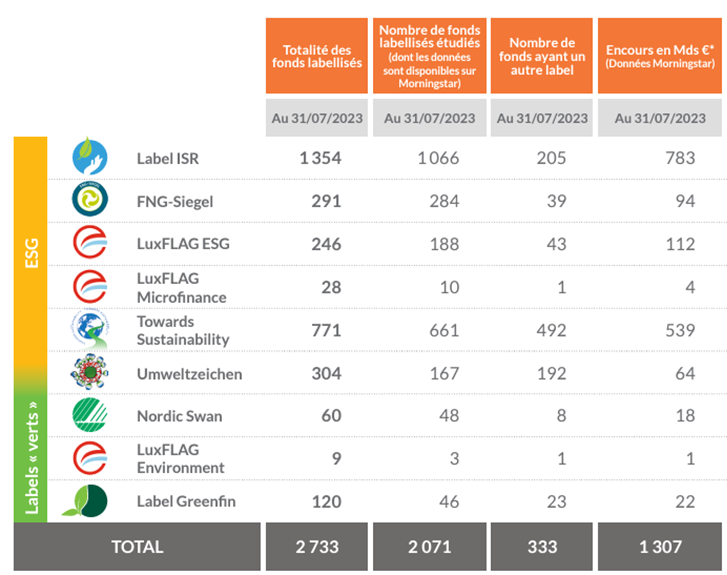

By July 31, 2023, the European market boasted over 2,000 funds with the "sustainable" label, managing assets in excess of €1,307 billion. Despite a significant outflow in 2022, the seven main European labels collected over 28 billion euros that same year, including 14 billion for SRI-labeled funds.

What are the main European labels and their characteristics?

In the European sustainable investment ecosystem, labels play an essential role in enabling investors to compare financial products and choose those that correspond to their values. The European market for sustainable finance labels is diverse and dynamic, each meeting specific needs:

- SRI label (France) : Attests that funds integrate ESG (Environment, Social and Governance) criteria into their investment decisions, guaranteeing responsible and transparent management that takes into account societal and environmental impact.

- Greenfin label (France): Focusing on environmental issues, this label certifies funds investing in projects with a positive impact on the energy and ecological transition.

- Finansol label (France): Designates solidarity savings products that finance projects with high social impact, such as financial inclusion and sustainable development in emerging countries.

- FNG-Siegel (Germany, Austria, Switzerland): Encourages a global ESG approach and rewards managers who integrate these criteria into all their activities, with an emphasis on transparency.

- Towards Sustainability (Belgium) : Emphasizes rigorous ESG analysis and excludes controversial sectors such as coal and unconventional fossil fuels.

- LuxFLAG (Luxembourg) : Offers several thematic labels (microfinance, climate, green bonds, etc.), targeting positive-impact projects.

- Umweltzeichen (Austria) : Certifies projects that reconcile economic performance with respect for the environment, encouraging sustainable practices.

These sustainable investment funds have made a name for themselves in theemployee savings market, where their adoption has been accelerated in France by legislation promoting the transition to a low-carbon economy, such as the Green Industry Act. They enable employees to invest in a variety of projects, from group retirement savings plans (Plan d'épargne retraite collectif au (PERO)), while generating a positive impact on society and the environment.

End of July 2023

(source : Novethic)

France leads the way in SRI in Europe

The most widely used labels are the French SRI label and the Belgian Towards Sustainability standard. In July 2023, the SRI label managed 783 billion euros of assets in 1354 funds, compared with 539 billion for Towards Sustainability, which had 771 label funds.

With the new SRI guidelines , which tighten up the conditions for certification, only 940 funds will retain the label as of January 1, 2025. Nearly 30% of previously-labeled funds will no longer qualify for the SRI label, as they fail to meet the new requirements.

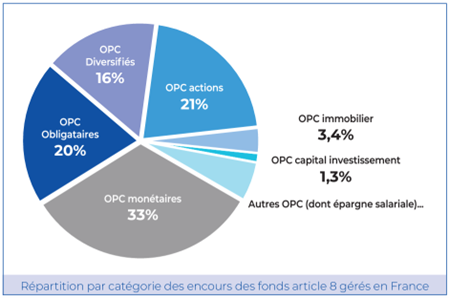

The majority of European label funds are classified as Article 8 under European SFDR regulations, with 80% of funds classified as Article 8 and 20% as Article 9. The Nordic Swan and Greenfin labels are mainly awarded to Article 9 funds.

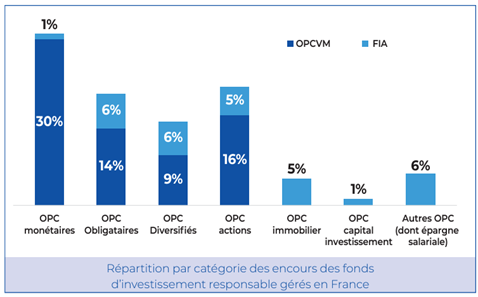

In France, sustainable investment in these funds reflects genuine diversification between different asset classes.

Responsible investment funds by asset class

The strategies behind SRI

Socially responsible investment (SRI) is based on a variety of strategies that combine ESG criteria with specific approaches:

Best" approaches:

- Best-in-class: Selection of the best ESG-rated companies by sector

- Best-in-universe: Identification of the best-performing companies on ESG criteria, across all sectors.

- Best-effort: Focus on companies improving their ESG practices

Exclusions :

- Sectoral: Elimination of sectors deemed harmful

- Normative: Exclusion of companies that do not comply with certain international standards

Active shareholder engagement :

- Investors influence ESG policies through their voting rights

Thematic approaches :

- Investment in specific themes such as healthcare or renewable energies

Impact investing :

- Combines financial return with measurable social or environmental impact

Excluding fossil fuels: a divisive approach

Within this complex landscape, the question of excluding fossil fuels remains central. Labels like Towards Sustainability take a strict approach, systematically excluding coal and unconventional oil and gas. They defend the idea that any investment in these energies runs counter to global climate objectives.

Others, such as the French SRI label, preferred until very recently to maintain a more nuanced strategy, considering it essential to support major energy companies in their transition to sustainable investments, rather than excluding them. While this approach recognizes the complexity of the energy transition, it also raises questions about its effectiveness and consistency with climate commitments.

The recent evolution of the French SRI Label (in March 2024), with the inclusion of a climate dimension in its base, excluding companies that exploit coal or unconventional hydrocarbons, bears witness to the need for greater consistency between the objectives of labels and the reality of investments.

Financial performance through the prism of sustainability

The impact of these divergences is reflected in the performance of sustainable investment funds. In 2022, the latter recorded an average decline of -14.09%, largely due to their low exposure to fossil fuels, a sector that enjoyed strong growth against the backdrop of the energy crisis. However, the beginning of 2023 showed a reversal of this trend, with average performances reaching +13.52%.

These fluctuations highlight the need to adopt a long-term perspective. While the exclusion of fossil fuels may penalize short-term performance, it is in line with a logic of climate risk management, anticipating future regulations, consumer preferences and the impact of climate change on businesses.

Green taxonomy: an essential compass

To navigate this complex universe, the European green taxonomy plays a key role. This classification system provides a framework for identifying genuinely sustainable economic activities and avoiding the abuses of greenwashing [1]. By demanding greater transparency, it helps investors distinguish between funds that are genuinely committed to the ecological transition and those that merely capitalize on the craze for sustainable and responsible investment.

However, Morningstar's study reveals that the majority of labelled funds (93%) in Europe are not aligned with this taxonomy, raising questions about the effectiveness of current labels.

A reform of these labeling frameworks therefore seems essential to restore investor confidence.

Striking a balance for sustainable investment

Sustainable investment is at a turning point. The growing demand for responsible investment reflects a collective awareness, but is accompanied by high expectations, both in terms of transparency and real impact.

Excluding fossil fuels remains a controversial approach, but it sends a strong signal in favor of a low-carbon economy. At the same time, tools such as the green taxonomy offer an essential compass to guide investors in their choices.

To build a truly sustainable future, it is imperative to strengthen consistency between labels, encourage transparency and promote a long-term vision.

[1]

What is greenwashing?

Greenwashing is a deceptive practice in which a company gives the impression that its products or actions are more environmentally friendly than they really are. This can include the use of vague terms such as "ecological" or "sustainable" without concrete evidence, or the use of nature imagery to suggest a positive environmental impact.

Basically, it's a way for some companies to give themselves a green image without actually adopting sustainable practices. This can mislead consumers into buying products they believe to be more environmentally friendly than they actually are.

FAQ - Questions about sustainable investment

Article écrit par

Amadou Kasse

Damien Vieillard-Baron

Damien Vieillard-Baron

Margaux Vieillard-Baron

Margaux Vieillard-Baron

Amadou Kasse

Amadou Kasse

Estelle Baldereschi

Estelle Baldereschi