Socially Responsible Investment (SRI): illusion or reality?

Rédigé par Amadou Kasse Publié le 22/11/2024

Partager

Socially responsible investment (SRI) is on a roll. SRI fundswhich integrate environmental, social and governance (ESG) criteria into their investment decisions, are winning over a growing number of investors. But behind this dazzling growth lie many nuances and questions. This decryption offers an in-depth analysis of the SRI universe, based on the latest data and comparing the promises of this market with the realities of investment.

The meteoric rise of SRI and the SRI label

The figures speak for themselves. SRI funds have experienced spectacular growth in recent years, reflecting investors' growing interest in sustainable investment. They have largely penetrated the employee savingsalso known as green savingsoffering employees the possibility of investing in projects, via Collective Retirement Savings Plans (PERCO) orMandatory Retirement Savings Plans(PERO), that have a positive impact on society and the environment.

The emergence of a number of labels, including the SRI label, has helped to structure the market and provide investors with a clearer picture of what's available.

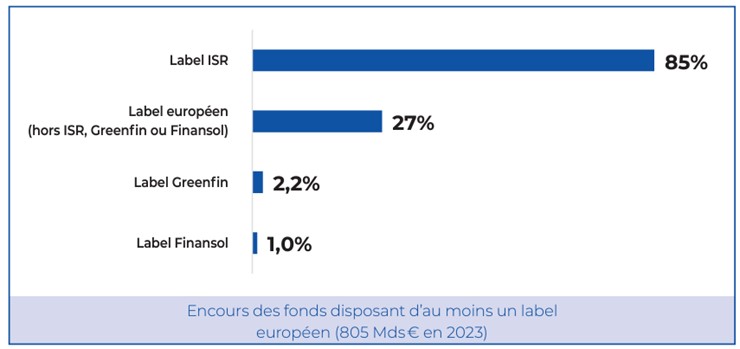

In 2023, the outstandings of the 1037 funds managed in France with at least one label, amounted to 805 billion euros.€. Of these 85% carried the SRI labellabel, while the Greenfin and Finansol labels accounted for 2.2% and 1% of assets under management respectively.

The SRI label: a performance driver or just a marketing argument?

One of the main questions surrounding SRI concerns financial performance. Contrary to popular belief, investing in SRI-labeled funds does not mean giving up on profitability.

SRI is not an end in itself, but a means of promoting positive corporate transformation. SRI funds invest in companies committed to a virtuous approach, while recognizing that no company is perfect.

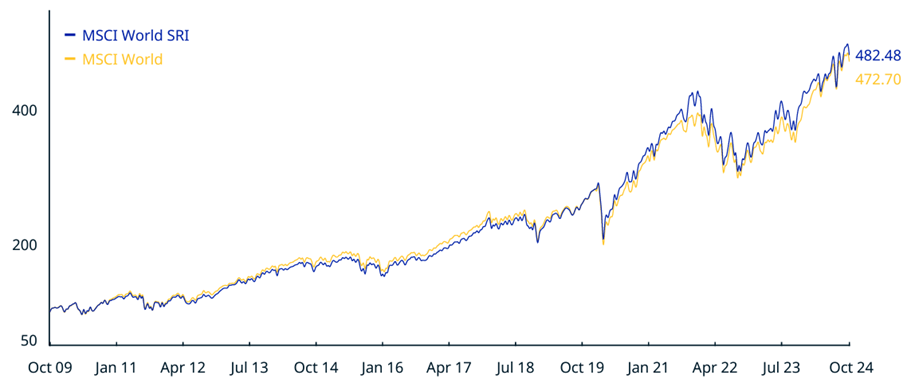

How do SRI labels perform?

Numerous studies show that the performance of SRI funds is comparable, or even superior, to that of traditional funds over the long term. These results can be explained by the fact that ESG risks are taken into account, which can have an impact on company performance.

Comparison of SRI and non-SRI funds

Cumulative gross performance of the MSCI World SRI index [1]from 2009 to 2024

What regulations are needed to clarify these SRI labels?

This has prompted legislators to crack down on the meteoric growth of these funds. To control this dynamic, they have introduced initiatives such as the European Sustainable Finance Disclosure Regulation ( SFDR ). It provides greater transparency on sustainable financial products and enables investors to better understand the characteristics of SRI funds.

In 2023, 59% of funds and mandates under management in France were classified under articles 8 or 9 of these regulations, reflecting the growing adoption of responsible investment.

- Article 8: includes funds with environmental or social characteristics.

- Article 9: includes funds with sustainable investment objectives.

The SRI label, for its part, acts as a valuable indicator, although it is not exempt from criticism, particularly with regard to greenwashing. This has led the French Ministry of the Economy to introduce new specifications for asset management companies wishing to use the SRI label, in order to better distinguish the wheat from the chaff.

Challenges and limits of the SRI label

SRI, while attractive, is no panacea. While SRI funds offer an interesting alternative for investors concerned about the environment and society, their implementation raises a number of questions. Indeed, the reality of responsible investment is more complex than it seems. This is particularly true in the context ofemployee savings schemes, where employees, often less well-informed than professional investors, may have high expectations of SRI-labelled funds.

Beware of greenwashing

Despite the guarantees offered by the SRI label, the risk of greenwashing remains a major concern. It is essential to be wary of claims that are too good to be true, and to give preference to funds whose investment policy is transparent and rigorous.

SRI does not mean investment security

Not all SRI funds have the same strategic approach. Some exclude the most controversial sectors, while others favor dialogue with companies to encourage change. Their risk profile also varies according to the investment choices made by the fund managers. This diversity makes risk and impact assessment a complex task.

Complexity of ESG criteria

The ESG criteria criteria are many and varied, making it difficult to compare funds. It's important to understand each fund's specific criteria before investing.

Even if SRI SRI funds can have a positive impacttheir transformative power should not be overestimated. Environmental and social challenges are complex and require action at all levels of society.

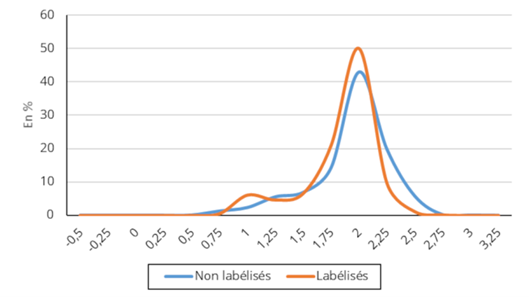

The limits of the SRI label

"SRI-labelled funds are not "green" in absolute terms, but they are "greener" than non-labelled funds".

The SRI label, while a useful indicator, is not enough to guarantee a truly sustainable investment. Indeed, while SRI-labeled funds are on average less carbon-intensive, a significant proportion of their investments remain exposed to environmental risks. The label acts more as a filter to exclude the worst performers than as a guarantee of environmental excellence.

Distribution of funds according to the average carbon intensity2 of their portfolio

Source: Banque de France, ISS.

How can SRI be integrated into an investment strategy?

Responsible investment is a personal choice that must be part of an overall investment strategy. It's important to understand your objectives and constraints before taking the plunge.

To reduce risk, it is advisable to diversify your investments by choosing several SRI funds with different characteristics or asset classes. In addition, there are a number of different labels for reconciling financial performance with social and/or environmental performance. A diversified offering should also include a wide range of labels that meet a variety of objectives

Investors must demand maximum transparency from fund managers. They must have access to clear and precise information on ESG criteria, stock selection methodology and the results obtained.

Last but not least, regulatory authorities must continue to step up requirements in terms of transparency and the fight against greenwashing.

What are the ambitions of the new SRI label?

At the end of 2023, the French Ministry of the Economy and Finance unveiled a revised, more ambitious version of the SRI label. This new standards, which came into force on March 1, 2024 aims to meet the growing expectations of savers and today's environmental challenges, in particular the fight against climate change.

The new SRI guidelines include some notable changes:

- Exclusion of fossil fuels: The new label now excludes companies exploiting coal or unconventional hydrocarbons, as well as those involved in new hydrocarbon exploration, exploitation or refining projects.

- Transition strategies: Management companies will be required to analyze and implement transition strategies for portfolio companies, aligned with the Paris Agreement. By 2026, 15% of portfolios invested in high-impact sectors will have to have transition plans in line with this agreement, with a commitment for a further 20% to follow within three years.

- More stringent ESG criteria: The label will be more selective, excluding the 30% of companies with the lowest ESG ratings, compared with 20% previously. Greater transparency on the weighting of environmental, social and governance criteria will also be introduced.

- Ambitious climate policy and generalist approach: While focusing on the climate, the label retains its generalist character, with greater selectivity on other ESG criteria. Management companies will have to limit the negative impact of their investments.

Outlook for SRI and the SRI label

SRI offers a unique opportunity for investors, and therefore for companies, to reconcile financial performance with positive impact. However, it is essential to approach this market with a critical eye, and not to be seduced by promises alone. By adopting an enlightened approach and choosing rigorously selected funds, investors can help shape a more sustainable future.

You can also call on our experts to advise you on the appropriate financial management of your employee and retirement savings schemes .

As a company with a mission, these issues are an integral part of our approach, and thanks to our ESG (Environment, Social, Governance) guidelines, we enable each customer to choose an insurer that corresponds to the values and sensitivities of their employees.

[1] The MSCI World SRI index selects the world's best companies in terms of ESG criteria, excluding those with a negative impact. It offers investors exposure to a geographically diversified and responsible basket of equities.

[2]Carbon intensity is defined as carbon dioxide emissions per unit of energy. The score measures the greenhouse gas emissions associated with the production, distribution and consumption of a fuel.

Article écrit par

Amadou Kasse

Damien Vieillard-Baron

Damien Vieillard-Baron

Margaux Vieillard-Baron

Margaux Vieillard-Baron

Amadou Kasse

Amadou Kasse

Estelle Baldereschi

Estelle Baldereschi