Focus on the PLFSS 2025 for supplementary pensions

Rédigé par Amadou Kasse Publié le 15/11/2024

Partager

PLFSS 2025 and retirement: what are the challenges and solutions for companies?

The Social Security Financing Bill (PLFSS) for 2025 marks a decisive step towards restoring France's public finances, with major measures aimed at preserving the social protection model.

Here's an overview of the key measures designed to guarantee the future of our supplementary pension system and strengthen the rights of self-employed workers.

1 Reducing the public deficit: an ambitious goal for retirement in the PLFSS 2025

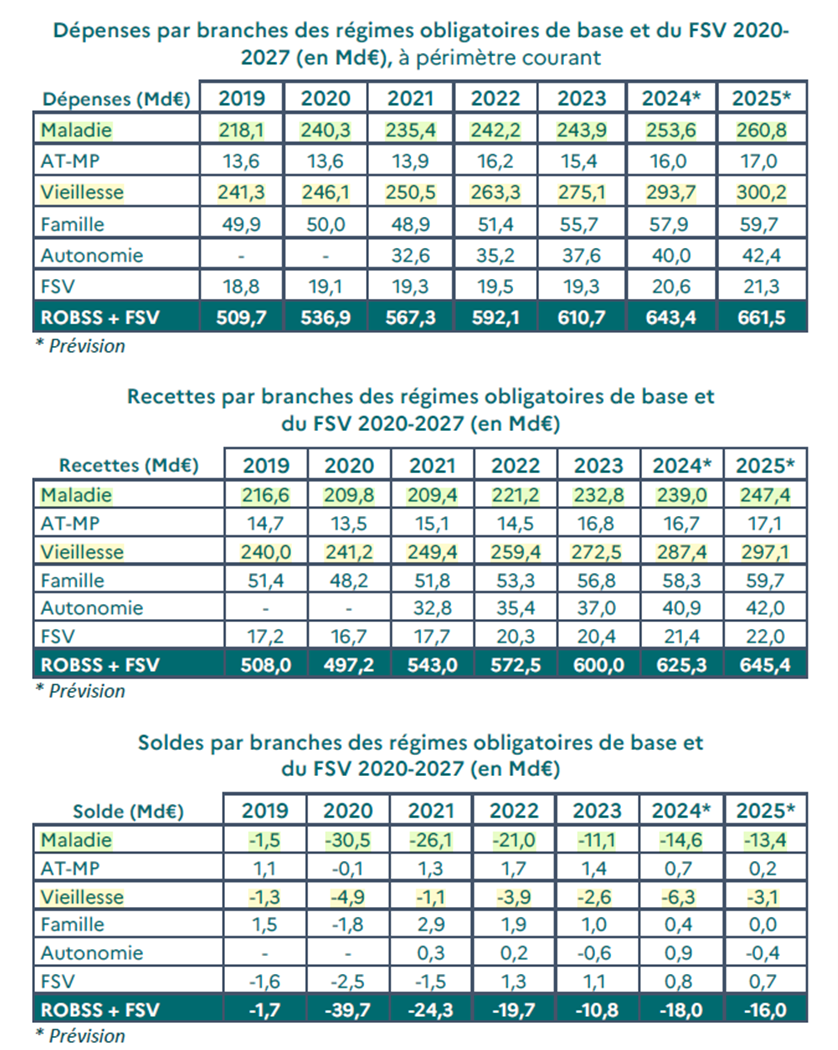

Faced with a public deficit that could reach 7% of GDP by 2025, the PLFSS 2025 commits to reducing this figure to 5%. This effort, which concerns all public administrations, includes Social Security, which accounts for around half of public spending. The aim is to preserve social protection for the French, while guaranteeing its financial sustainability.

All in all, an effort of 60 billion euros needs to be made, across all areas of public action.

2. Controlling pension expenditure: adjustments and savings

Structural reforms, such as the pension reform in 2023, are producing financial effects, estimated to improve the balance of all pension schemes by nearly 4 billion euros, but these effects are gradual, and additional efforts are still needed today to absorb the social security deficit.

Pensioners are being asked to make an effort as part of measures to control social spending. Initially, the Social Security Financing Bill (PLFSS) for 2025 planned to shift the revaluation of retirement pensions from January 1 to July 1. This measure would have saved an estimated 4 billion euros in 2025 by freezing pensions at their current level for the first half of the year, while limiting the increase in social spending.

In the face of criticism, the government has opted for a compromise. From now on, all pensioners will benefit from an increase in their pension from January 1, but at a rate equivalent to half the estimated inflation, i.e. an increase of 0.9% in 2025.

Pensioners receiving a pension of less than the SMIC net monthly income (1,426 euros) remain protected, however.

At the same time, the increase of 4 points per year in the contribution rate paid by local authority and hospital employers to the Caisse Nationale de Retraite des Agents des Collectivités Locales (CNRACL) will kick-start the recovery of this structurally-deficient scheme, and bring in 2.3 billion euros in additional revenue for the old-age branch.

3. Ensuring the viability of the pay-as-you-go pension system: focus on the PLFSS 2025

The PLFSS 2025 implements several reforms to improve pensions for the self-employed. From January1, 2025, a new basis for calculating social security contributions for the self-employed will come into force, promoting the creation of better pension rights for the self-employed. In addition, the calculating pensions fornon-salaried agricultural workers will be aligned with that of the general scheme, to guarantee fairer and more equitable pensions.

Secondly, with the aim of preserving the balance of the pension system, the PLFSS 2025 is based on the assumption that the accounts of the CNRACL, which covers civil servants in the local and hospital civil services, will be rebalanced. By 2030, the CNRACL will have a deficit of almost 10 billion euros, or two-thirds of the total deficit of the old-age branch.

This pension fund is facing a growing deficit, due in particular to the deterioration in the demographic ratio between contributors and pensioners. To ensure the financial viability of CNRACL, a gradual increase in employer contribution rates will be implemented from 2025 to 2027, with an initial rise of 4 points in 2025.

4. Strengthening the pension rights of self-employed workers: what progress has been made?

The PLFSS 2025 also includes specific measures for farmers. The system of exemption from employer contributions for seasonal workers will be made permanent, and the ceiling on remuneration giving rise to total exemption will be raised. These measures are designed to boost the competitiveness of the agricultural sector and support the installation of young farmers.

These adjustments strengthen the pension rights of self-employed workers, while helping to balance the overall pay-as-you-go pension system in the face of the challenges posed by an ageing population.

A compulsory system under pressure: why does the PLFSS 2025 encourage companies to plan complementary solutions?

The Social Security Financing Bill for 2025 (PLFSS 2025) tackles a persistent problem: the unbalanced imbalance of the pay-as-you-go system.

It highlights the financial difficulties of the pay-as-you-go pension scheme, which is under pressure from an aging population and rising life expectancy.

Although the proposed adjustments are designed to guarantee the system's long-term viability, they could ultimately weaken the purchasing power of retirees and make the pension paid by the compulsory scheme insufficient to guarantee a decent standard of living, especially for the most modest wage earners. Faced with the challenges highlighted by the PLFSS 2025 and the growing fragility of the pay-as-you-go pension system, it is essential for companies to anticipate and offer additional retirement savings solutions.

Schemes such as the Retirement Savings Plan (PER) or other retirement savings schemes can offer employees additional security. Complementing the PLFSS 2025 retirement measures, these savings solutions represent a strategic means of ensuring a better financial future for employees and retaining talent within the company.

For more details on the provisions of the PLFSS 2025, consult the press kit on the Ministry of the Economy website

You can also find out what's likely to change for companies in terms of health and personal protection: PLFSS 2025: What changes for companies?

Article écrit par

Amadou Kasse

Damien Vieillard-Baron

Damien Vieillard-Baron

Margaux Vieillard-Baron

Margaux Vieillard-Baron

Amadou Kasse

Amadou Kasse

Estelle Baldereschi

Estelle Baldereschi