Euro fund dynamics put to the test by the markets

Rédigé par Amadou Kasse Publié le 21/02/2025

Partager

A mixed picture for euro funds in 2024

The year 2024 was marked by major political and economic events, with significant repercussions on financial markets, particularly on euro funds. In France, the dissolution of the National Assembly on June 9, announced by the President of the Republic, led to a political crisis that weighed heavily on French equities.

After setting an all-time record at 8259.19 points in May, the CAC 40 index ended the year down 2.1% at 7381.26 points, while other European indices such as Germany's DAX (+18.85%) and Spain's IBEX 35 (+15%) posted remarkable performances.

Internationally, the year was characterized by a generally positive performance, driven by a gradual decline in interest rates, an economic recovery in China and the rise of innovative sectors such as green technologies and artificial intelligence.

Why are euro funds still a safe investment choice in 2024?

Euro funds remain a preferred option for savers seeking security and yield. However, returns on euro funds vary according to insurer or asset manager and investment strategy.

Strategic change in central bank monetary policies

The year 2024 was marked by a strategic shift on the part of the major central banks, aimed at reviving global economic growth after a period of tightening.

- ECB: The European Central Bank reduced its deposit rate to 3%, signalling a more accommodating policy to support the eurozone economy. This decision particularly benefited cyclical stocks, such as the automotive industry and European banks, boosting market liquidity and the attractiveness of safe-haven investments.

- FED: In the United States, the Federal Reserve also continued to cut rates, supporting investment in growth stocks, particularly in the technology and consumer sectors, and encouraging investment in equities and bonds.

These decisions stimulated liquidity in the markets, encouraging a recovery in investment. However, they also rekindled inflation concerns, limiting investor confidence in certain sectors.

Performance of the main stock market indices in 2024

| IndexStock market indices | Change 2024 | Other financial instruments |

|

-2,15 % |

|

|

+18,85 % | |

|

+8,34 % | |

|

+23,33 % | |

|

+5,69 % | |

|

+19,22 % | |

|

+12,67 % |

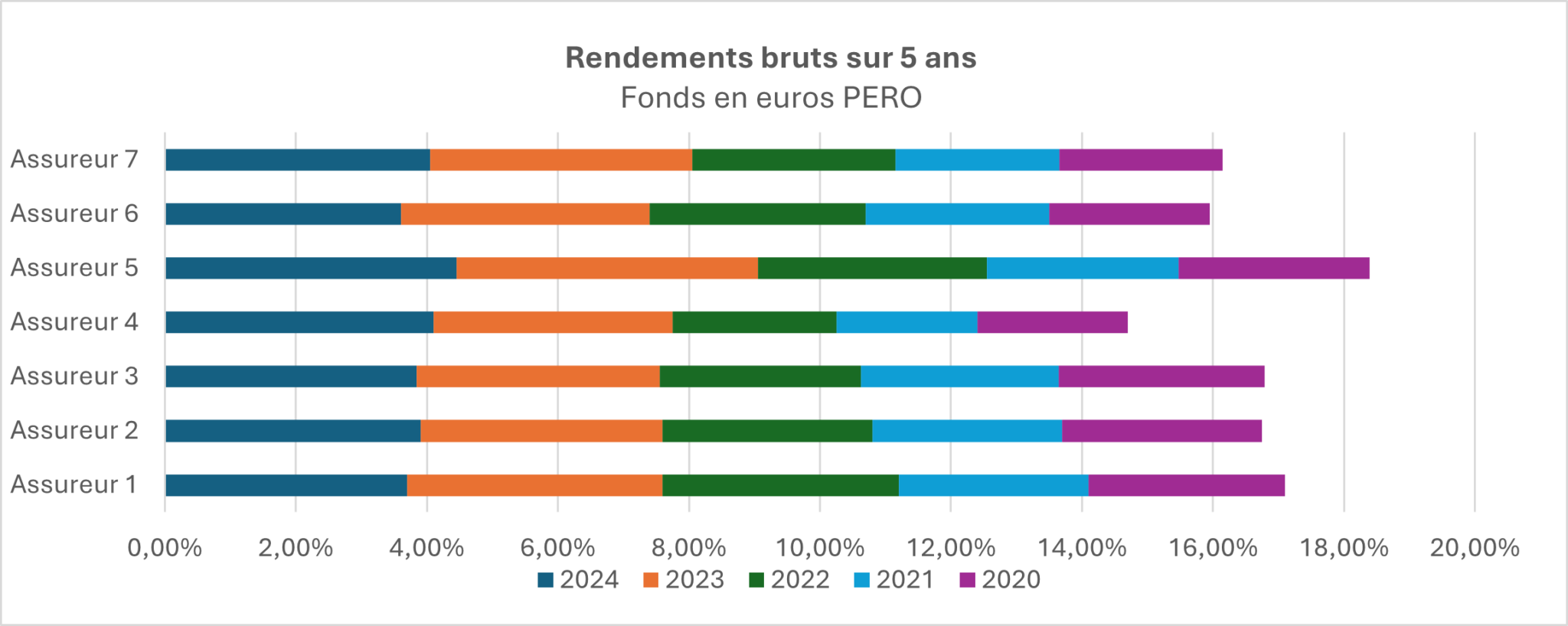

2024 returns on euro funds - PER Obligatoire

What are the best returns on insurers' euro funds in 2024?

An analysis of the yields of the main insurers' euro funds for mandatory RSPs reveals a general upward trend in the rates paid.

In 2024, rates of return on compulsory PER euro funds will range from 3.60% to 4.45% gross, with average performance exceeding that of previous years. Among the best-performing insurers in 2024, two in particular stand out thanks to a more pronounced revaluation policy, with gross returns of 4.45% and 4.10%.

Over a five-year horizon, cumulative performances reveal significant differences between insurers, with the best cumulative return at 19.78%, representing an annualized return of +3.68%, and 15.57% for the lowest of the 7 insurers observed (+2.94%/year).

What factors influence returns on euro funds?

It is important to stress that these performances must be interpreted in the light of each insurer's own policy and investment conditions.

In fact, the return on the euro fund depends heavily on the proportion of savings invested in unit-linked products (UC): insurers favor contracts with greater exposure to UC.

In addition, each insurer's own financial management policy (asset allocation, profit-sharing provisions, revaluation policy) also plays a key role in influencing performance, not to mention the administrative management fees that will be deducted from these observed returns (fees have a direct impact on the net return received by the saver).

🔗 Also read: Understanding the PER Obligatoire (PERO)

Forecasts for 2025: what does the future hold for euro funds?

Opportunities and risks

According to the consensus, the economic outlook for 2025 reveals contrasting dynamics by region.

- North America: In the USA, economic growth is set to slow and stabilize at around 1.6%, marked by a weakening labour market and public spending. However, household consumption, underpinned by moderate real wages, could provide a foundation of resilience.

- Europe: The eurozone is facing heightened trade tensions, particularly with the United States. Economic growth is expected to reach 1%, with opportunities for fiscal stimulus in Germany to boost domestic demand.

- Emerging markets: Institutional investors are optimistic about emerging markets, particularly Asia ex-China and India, which is expected to surpass China as the main investment destination. Economic growth in these regions should be underpinned by increased demand and relaxed monetary policies (> 5%).

Interest rate trends and impact on euro funds

For 2025, monetary policy forecasts anticipate a further reduction in key rates, against a backdrop of slowing inflation.

- The ECB could reduce its key rate to between 1.75% and 2% by the end of 2025, compared with 3.15% at the end of 2024.

- The FED is reportedly considering a key rate range of between 3.50% and 3.75%, compared with levels above 4.25% in 2024.

These adjustments should continue to support financial markets. This reduction could also make funds more attractive in 2025, thereby creating a more favorable environment for businesses and households, by providing stable returns for the various mandatory life insurance and/or PER contracts.

The year 2025 promises to be rich in opportunities, but also marked by sectoral and geopolitical risks. The varied performance of regions and sectors underscores the importance of a diversified strategic approach. While green technologies, artificial intelligence and emerging markets continue to capture investors' attention, uncertainties remain over the impact of protectionist policies in the USA and global trade tensions.

The dynamic trend in returns on compulsory RSP euro funds shows an upturn in secure investment solutions. This upturn is taking place against a backdrop of more favorable interest rates, but it should not obscure the disparities between insurers and the structural evolution ofretirement savings contracts.

Disclaimer: The information contained in this article is based on prospective studies carried out by asset management companies and institutional investors. It does not constitute an investment recommendation and is not binding on Gerep.

Need support? Contact a Gerep expert to optimize your savings or optimize your contracts by auditing your existing schemes.

FAQ: frequently asked questions

What is a euro fund?

A euro fund is an investment vehicle offered in life insurance contracts. It is mainly made up of bonds, offering a high level of capital security. Its main advantage is that it guarantees the capital invested and generates interest every year, although the return may vary according to the performance of the financial markets and the insurer's management.

What is a unit of account?

A unit of account (UA) is an investment medium available in multi-support life insurance contracts. Unlike the euro fund, it does not guarantee capital, as it is invested in a variety of assets such as equities, bonds or real estate funds. The aim is to achieve a higher potential return over the long term, but with a risk of capital loss depending on market trends.

Should you invest in euro funds in 2025?

Euro funds are still the right choice for investors seeking security and stable returns. However, it is essential to choose your contract carefully, taking into account fees, units of account and past performance.

Article écrit par

Amadou Kasse

Damien Vieillard-Baron

Damien Vieillard-Baron

Margaux Vieillard-Baron

Margaux Vieillard-Baron

Amadou Kasse

Amadou Kasse

Estelle Baldereschi

Estelle Baldereschi