[EDITION 5]: Barometer of COVID-19 impact on medical consumption

Rédigé par Margaux VB Publié le 31/01/2021

Partager

2020 REVIEW: Gerep’s vision was the right one!

What are the “medical consumption” effects of this health crisis on the healthcare economy?

Optics, dental care, routine care… how have the demands of the major categories changed?

GEREP, a group life and health insurance brokerage and management company, has been monitoring the impact of the health crisis on the medical consumption behavior of its policyholders throughout 2020, through regularly published barometers.

These independent, agile studies have enabled Gerep to anticipate the impact of the pandemic in terms of the different phases of containment and decontainment throughout 2020.

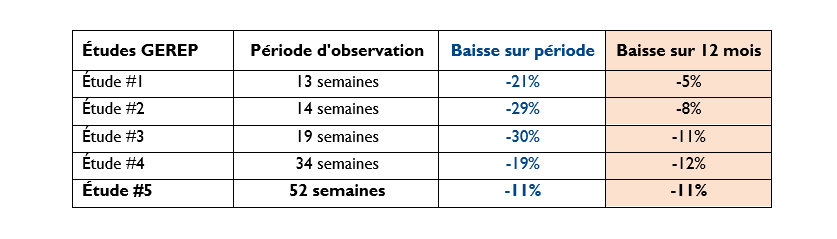

Through 4 studies published in the course of 2020, in April, May, June and October respectively, Gerep is today drawing up an annual review based on its expertise and its own experience, from which its customers have benefited as they look ahead to 2021. Gerep was right: the barometer confirms the initial projections of an 11-point reduction in consumption by 2020, whereas the market consensus was for a 5-point reduction.

The previous study showed a recovery initiated “post-containment” and projected an annual estimate of underconsumption due to Covid. Now, at the start of the year, it is possible to know the almost definitive landing. It is also interesting to see the weekly figures for the evolution of mediaconsumption.

Brief review of results from the first containment and previous studies

Studies #1 and #2 focused on the first weeks of the year before and during the first confinement.

Study #3 focused on the complete analysis of the first containment period (March 17, 2020 to May 11, 2020). Over this period, the change in medical consumption observed was -61% (over a 9-week period).

In addition to an overall analysis, the items that usually account for an average of 80% of total expenditure (Optical, Dental, Consultations/Visits, Hospitalization and Pharmacy) also gave rise to comments.

Notable features included :

- Optics and dentistry: the drop observed was over 90% over these 9 weeks of the first confinement with a total absence of reimbursement (100% drop over the week of April 12 to 18, 2020);

- Over the last few weeks of observation and after confinement: a more marked recovery in dental than in optical;

- A pronounced decline, albeit to a lesser extent, in consultations and visits, thanks in particular to the widespread use of teleconsultation;

- Good maintenance of the pharmacy for obvious reasons of continuity of care.

In the end, our various studies produced the following figures:

- Studies #1 and #2: we had anticipated a greater degree of catch-up than was finally observed;

- Studies #3 and #4: we have corrected our projections to arrive at a fairly good landing estimate (-11%).

Main conclusions of the “consumption” impact on supplementary health insurance

After studying all medical procedures without distinction, we looked at reimbursements for consultations, optical frames and dental prostheses.

A sharp decline in healthcare benefits: -11% over the 2020 vs. 2019 study period

The question was about the level of “partial catch-up”, which is now known. Finally, at portfolio level, if we consider all procedure families, it appears that the drop in medical consumption linked to the confinement period has not been fully made up. However, a recovery of around +9% has been observed since November.

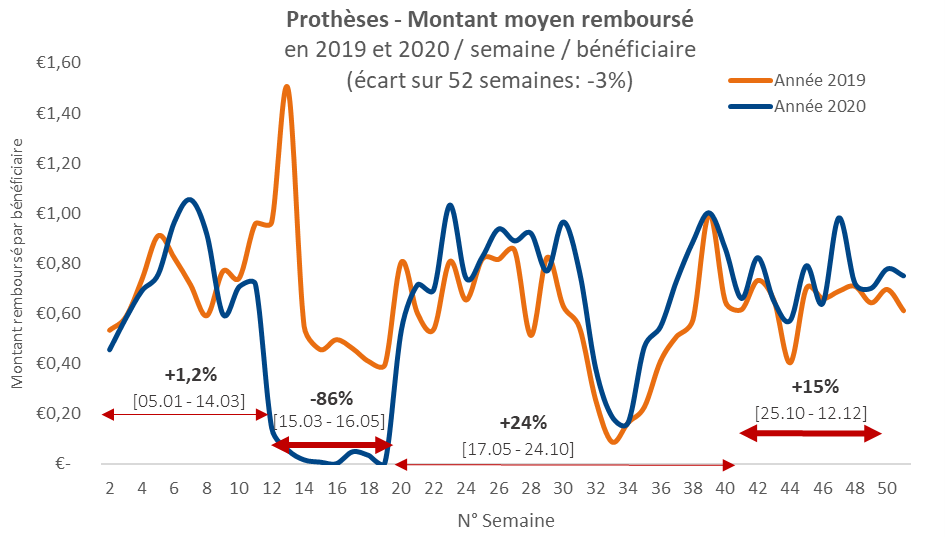

1. Optical sector: -34% over the period studied 2020 vs 2019

A first level of decline, certainly linked to the implementation of the 100% Healthcare reform, is first observed at the beginning of the year (-37% on average) before a vertiginous drop of 85% in medical consumption during the 1st containment period.

The study shows that, while there has been some catching up, this has been “masked” by the impact of the price cap (-37% and -13% for periods outside confinement).

As a reminder, the optical sector saw the start of 2020 marked by the effective implementation of the so-called “100% Health” reform: optical frames are capped at €100 in 2020, compared with an average of €150 in 2019.

This decline is structural and will continue throughout 2020. Finally, in the specific case of frames, the consumption gap is -34% for 2020 compared to 2019, in line with the trend observed in early 2020 before the confinement.

2. Dental: -3% over the period studied vs 2019 (January 1 to December 31, 2020)

Unlike optical frames, from January onwards, the application of the 100% health reform, which takes into account the position of the tooth and the material used for dentures, has had the effect of increasing reimbursements since the start of the year. Before the lock-in, the increase was 1.2%. The period of confinement, with the closure of dental surgeries, has wiped out spending.

Dental consumption is showing a marked upturn. An upward trend in consumption of around 24%, which has been fairly stable since May, shows a trend towards catching up.

This trend continued during the second, less restrictive period. However, it is still difficult to estimate the impact of the 100% health reform on this increase.

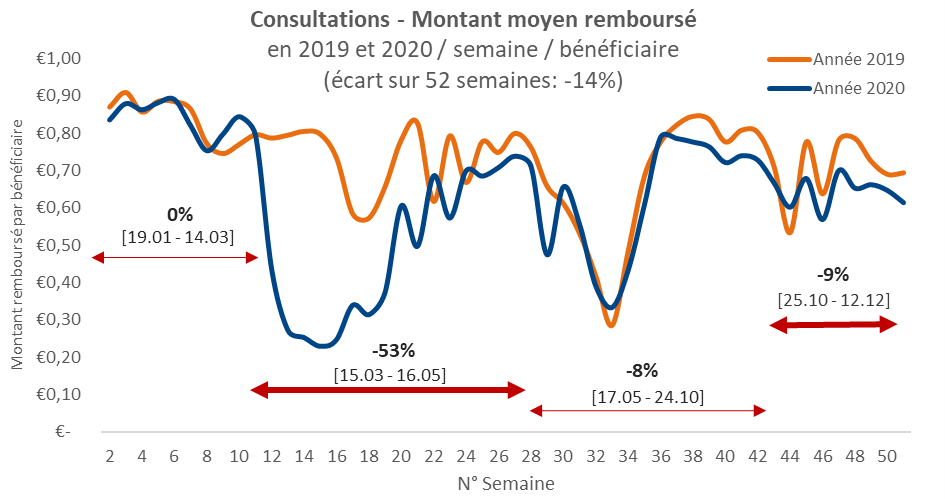

3. Consultations (general practitioners and specialists) : -14% over the study period 2020 vs 2019

Unlike the other two categories, optical and dental, consultations are not impacted by the 100% reform in the 2020 benefit comparison with 2019.

- The figure for the “before containment” period, -0.1%, shows stability on this item.

- The figure for the “1st confinement” period, -53%, is less severe than for optical frames and dentures. The explanation lies in teleconsultation, which worked well during the confinement period and is now widespread, both on the Social Security side and on the supplementary health insurance side.

- Finally, the “post-containment” figure reflects a partial return to normal:

- Urgent and necessary consultations took place during the confinement.

- Given the limited availability of doctors’ surgeries, a full catch-up seemed to make little sense.

Conclusion

In our last study (#4), we anticipated a partial catch-up, which is tending to be confirmed. The history of our forecasts (downward revaluation on an annual basis as our studies progress) clearly shows that the eventual “full” post-confinement catch-up is never equal to the decline.

In the end, only the first confinement had a remarkable effect on medical consumption.

The second confinement, between November1 and December 15, did not give rise to a second wave of “sharp” declines, but rather a slight echo of the first. This period was even marked by an upturn in consumption (+9.0% vs 2019), but this needs to be qualified: doctors’ consultations and optics remain “below” what is generally observed. Dental prostheses, on the other hand, are “above” the usual average, with “100% Santé” acting as a catalyst.

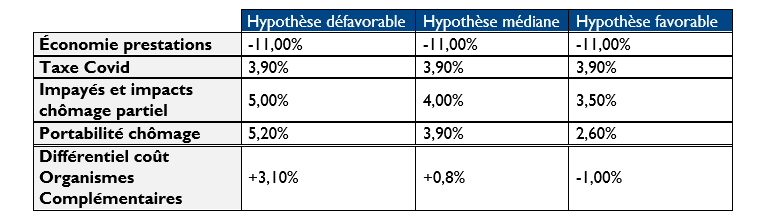

We have calculated the impact on complementary organizations for the year 2020:

TO REMEMBER :

- The Gerep barometer was right on target, in contrast to the overly cautious market consensus.

- 11% reduction in reimbursements by complementary organizations in 2020.

- This can be explained by the impact of the “responsible contract”, a “flat” year in optics, and the impact of the1st confinement, which has never been recovered.

- Real catch-up at the end of the year (last 10 weeks) on optical and dental care.

- The technical gain on the insurer’s side can only really be measured once the impact of unpaid contributions, short-time working and the future additional cost of portability of rights has been taken into account.

- With Gerep, companies benefit from an informed and independent view of how to negotiate and optimize their social protection budget with insurers.

You can read Issue 1 at this link

You can read edition 2 at this link

Article écrit par

Margaux Vieillard-Baron

Damien Vieillard-Baron

Damien Vieillard-Baron

Margaux Vieillard-Baron

Margaux Vieillard-Baron

Amadou Kasse

Amadou Kasse

Estelle Baldereschi

Estelle Baldereschi