Alert on the financial future of the pension system

Rédigé par Amadou Kasse Publié le 27/02/2025

Partager

The Cour des Comptes has just published the report of its audit detailing the financial situation of the French pension system and its short, medium and long-term prospects.

Despite successive reforms, the pension system is facing growing financial imbalances that could jeopardize its long-term viability. In fact, the deficit is worsening and threatening the long-term viability of the system.

An alarming report on the precariousness of the system

The French pension system: a fragmented structure marked by strong heterogeneity

The French pension system is characterized by its complexity and diversity, resulting from the multitude of schemes to which working people are obliged to contribute. This structure gives rise to significant heterogeneity between the financial situations of the various schemes. The result is a varied retirement landscape that is sometimes difficult to grasp.

The French system is based on several pillars:

- Basic schemes: compulsory for all working people

- Compulsory supplementary schemes: Agirc-Arrco for private-sector employees, Ircantec for contract employees

- Supplementary insurance or supplementary retirement (optional): individual and/or group retirement savings plans

This multi-level architecture contributes to the difficulty of managing the pension system. It also accentuates financial disparities between schemes, with no fewer than 42 different pension funds (basic and supplementary schemes combined).

Disparate financial situations

The Cour des Comptes has identified six main groups of schemes, each with its own organizational and financial specificities.

- The general scheme and the agricultural workers' scheme account for 42% of total pensions. Their financial situation remains precarious, with a deficit limited to 0.2 billion euros in 2023, but rising from 2024.

- The pension fund for local authority and hospital civil servants covers 7% of total pensions. It is facing a critical situation due to the rapid deterioration in the ratio of contributors to retirees, leading to a deficit of 2.5 billion euros by 2023.

- Plans for the liberal professions and lawyers benefit from a more favorable financial situation.

- The compulsory supplementary schemes, managed by the social partners and subject to specific rules, have seen a rapid turnaround in their financial situation, recording a total surplus of 9.9 billion euros in 2023.

- The special schemes comprise 17 schemes to which the State contributes 8 billion euros to ensure their financial equilibrium.

- Last but not least, the civil and military servants' scheme is partially funded by the State, with a contribution of 45 billion euros in 2023.

This diversity of schemes means that financial situations differ greatly. Some schemes, such as those for local civil servants and hospitals, are running substantial deficits. Others, such as the compulsory supplementary schemes, have significant surpluses, particularly Agirc-Arrco (€101.7 bn) and RAF.

The role of the State in financing the pension system

The French government plays a crucial role in financing the French pension system, contributing to the financial equilibrium of 17 special schemes and funding the schemes of civil servants and military personnel.

However, how these contributions are accounted for is a matter of debate. The State's apparent contribution rates for civil servants are significantly higher than those of private companies under the general scheme. Nevertheless, the structural differences between these systems make direct comparisons of little relevance.

Key figures for imbalance and projected deficit

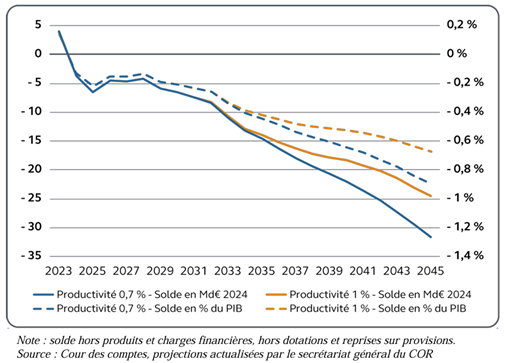

In 2023, the pension system will have a surplus of 8.5 billion euros, mainly thanks to the acceleration of inflation, which has increased tax revenues faster than expenditure.

However, this surplus is misleading:

- 2025: estimated deficit of 6.6 billion euros

- 2035: 15 billion euro deficit

- 2045: 30 billion euro deficit

The Cour des Comptes predicts a growing deficit over the coming years. By 2045, the general scheme's debt could reach 350 billion euros, while that of the CNRACL could amount to 120 billion euros.

This unfavorable outlook is set against a backdrop of continuing population aging. The ratio between the number of contributors and the number of pensioners will continue to fall, despite the increase in the average retirement age, from around 1.77 in 2025 to 1.66 in 2035 and 1.54 in 2045. Financing the pension system will therefore become increasingly critical.

Balance of pension system (in €bn and as % of GDP)

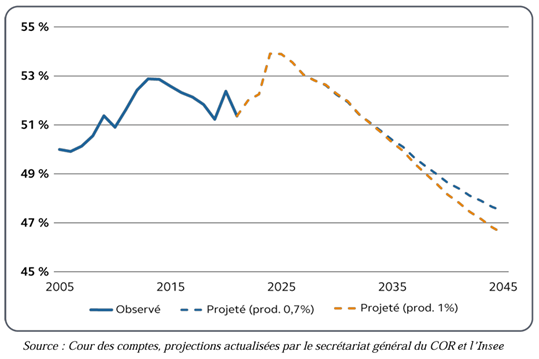

Average pension in relation to average earned income

The effects of past reforms

Since 2003, several reforms have been implemented to contain the rise in pension expenditure, the latest of which raised the legal retirement age to 64 and 172 quarters for a full pension.

These reforms have made it possible to raise the retirement age and increase the length of insurance required for a full pension.

In 2023, the average retirement age will be 62 years and 8 months, compared with 60 years in 2010.

These measures helped to temporarily improve the system's financial equilibrium.

How has the 2023 reform impacted the pension system?

The pension reform of 2023 has brought significant changes to the way people retire and how they receive their pensions.

One of the main measures is the gradual increase in the legal retirement age from 62 to 64, in response to demographic challenges and to guarantee the financial viability of the system. In addition, the length of insurance required to qualify for a full pension has been increased, reaching 172 quarters (43 years) for generations born from 1965 onwards.

- Positive financial effects in the short term: The reform has reduced pension expenditure and increased revenues by raising the retirement age and increasing contributions. By 2032, the number of pensioners should be 350,000 lower than without the reform.

- Temporary improvement in the balance: The reform has improved the balance of the pension system by 1.6 billion euros in 2025, with a peak improvement of 7.1 billion euros in 2032. However, this positive effect should gradually diminish after 2040.

- Impact on public finances: The reform has also had a positive impact on public finances, with an estimated improvement of 24.2 billion euros in 2030, taking into account additional revenues and savings.

Main reform levers identified by the Cour des Comptes

According to the Cour des Comptes, several levers can be used to restore the financial balance of the pension system:

- Age of entitlement: Raising the age of entitlement would reduce expenditure and increase revenue. For example, raising the age of entitlement by one year could improve the balance by 8.4 billion euros in 2035.

- Required insurance period: Increasing the insurance period required to qualify for a full pension would encourage people to work longer, thereby reducing pension expenditure. A one-year increase in the required insurance period could improve the balance by 5.2 billion euros in 2035.

- Resources from the working population: Increasing the social security contributions of working people would generate additional resources to finance pensions. A one-point increase in contributions could generate between €4.8 and €7.6 billion a year.

- Indexation of pensions: Changing the rules for indexing pensions to bring them into line with wage trends rather than inflation could help to better control pension expenditure.

However, the Cour des Comptes overlooked one crucial lever: collective capitalization.

Faced with the challenges of the pay-as-you-go pension system, collective capitalization is an effective and complementary response. It generates attractive returns, relieves pressure on assets and finances the real economy, creating a virtuous circle of growth and employment.

French players have already demonstrated their effectiveness. The ERAFP has accumulated 43 billion euros on behalf of civil servants, with an average yield of 4.2%. The Banque de France self-finances a large part of its employees' pensions through a 14-billion-euro fund. The Senate, with 1.4 billion euros invested, covers 55% of the pensions it pays out without asking taxpayers.

In countries that combine capitalization and pay-as-you-go schemes, such as Sweden and the Netherlands, pensions are more solid and predictable. The Cour des Comptes' oversight is therefore regrettable: developing capitalization is a necessity to guarantee the future of pensions.

Future choices will be decisive in preserving pensioners' standard of living and the system's equilibrium.

To find out more, don't hesitate tocontactour teams.

Article écrit par

Amadou Kasse

Damien Vieillard-Baron

Damien Vieillard-Baron

Margaux Vieillard-Baron

Margaux Vieillard-Baron

Amadou Kasse

Amadou Kasse

Estelle Baldereschi

Estelle Baldereschi